Healthcare Is A Taxing

Situation

Gary Gerard,

dumbhoosier.com

This week, in a largely symbolic gesture, the United States House of

Representatives repealed the health care measure passed by the last

Congress.

I say it’s symbolic because the Senate likely will not pass the bill

and even in the highly unlikely event that it did, the bill would

surely be vetoed by President Obama.

Nonetheless, I think the discussions of the healthcare bill remain

valid.

There are lots of reasons – constitutional and otherwise – to oppose

the flawed health insurance law that is commonly known as Obamacare.

But I want to focus this week on something that has not been at the

forefront of the discussion.

Aside from all its other flaws and foibles, Obamacare constitutes one

of the largest tax increases in history.

Americans for Tax Reform recently published a comprehensive list of tax

hikes in Obamacare. Following is a synopsis of their research.

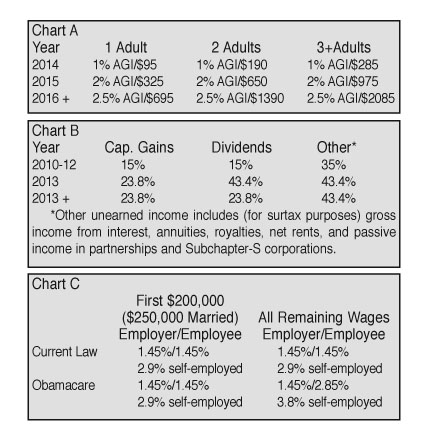

The charts that I refer to are on page 2A. The numbers are the month

and year the tax takes effect, followed by the amount the tax will

raise over 10 years.

Individual Mandate Excise Tax 1/14 – Starting in 2014, anyone not

buying “qualifying” health insurance must pay an income surtax, the

higher of the two figures in Chart A, where AGI is adjustible gross

income.

Employer Mandate Tax 1/14 – If an employer does not offer health

coverage, and at least one employee qualifies for a health tax credit,

the employer must pay an additional non-deductible tax of $2,000 for

all full-time employees. This provision applies to all employers

with 50 or more employees. If any employee actually receives coverage

through the exchange, the penalty on the employer for that employee

rises to $3,000. If the employer requires a waiting period to enroll in

coverage of 30-60 days, there is a $400 tax per employee ($600 if the

period is 60 days or longer).

(Combined, the individual and employer mandates will raise $65B.)

Surtax on Investment Income 1/13 $123B – This increase involves the

creation of a new, 3.8 percent surtax on investment income earned in

households making at least $250,000 ($200,000 single). This would

result in the top tax rates on investment income shown in Chart B.

Excise Tax on Comprehensive Health Insurance Plans 1/18 $32B – This is

a new 40 percent excise tax on “Cadillac” health insurance plans

($10,200 single/$27,500 family). For early retirees and high-risk

professions exists a higher threshold ($11,500 single/$29,450

family). CPI +1 percentage point indexed.

Hike in Medicare Payroll Tax 1/13 $86.8B – Current law and changes. See

Chart C.

Medicine Cabinet Tax 1/11 $5B – Americans no longer able to use health

savings account (HSA), flexible spending account (FSA), or health

reimbursement (HRA) pre-tax dollars to purchase non-prescription,

over-the-counter medicines (except insulin)

HSA Withdrawal Tax Hike $1.4B 1/11 – Increases additional tax on

non-medical early withdrawals from an HSA from 10 to 20 percent,

disadvantaging them relative to IRAs and other tax-advantaged accounts,

which remain at 10 percent.

Flexible Spending Account Cap – aka “Special Needs Kids Tax” 1/13 $13B

– Imposes cap of $2500 (Indexed to inflation after 2013) on FSAs (now

unlimited). There is one group of FSA owners for whom this new cap

will be particularly cruel and onerous: parents of special needs

children. There are thousands of families with special needs

children in the United States, and many of them use FSAs to pay for

special needs education. Tuition rates at one leading school that

teaches special needs children in Washington, D.C. () can easily exceed

$14,000 per year. Under tax rules, FSA dollars can be used to pay

for this type of special needs education.

Tax on Medical Device Manufacturers 1/13 $20B – Medical device

manufacturers employ 360,000 people in 6000 plants across the

country. This law imposes a new 2.3% excise tax. Exemptions

include items retailing for less than $100.

Raise "Haircut" for Medical Itemized Deduction from 7.5% to 10% of AGI

1/11 $15.2B – Currently, those facing high medical expenses are allowed

a deduction for medical expenses to the extent that those expenses

exceed 7.5 percent of adjusted gross income (AGI). The new

provision imposes a threshold of 10 percent of AGI; it is waived for

65+ taxpayers in 2013-2016 only.

Tax on Indoor Tanning Services 7/10 $2.7B – New 10 percent excise tax

on Americans using indoor tanning salons

Elimination of tax deduction for employer-provided retirement Rx drug

coverage in coordination with Medicare Part D 1/13 $4.5B.

Blue Cross/Blue Shield Tax Hike 7/10 $0.4B – The special tax deduction

in current law for Blue Cross/Blue Shield companies would only be

allowed if 85 percent or more of premium revenues are spent on clinical

services

Excise Tax on Charitable Hospitals (Min$/immediate) – $50,000 per

hospital if they fail to meet new "community health assessment needs,"

"financial assistance," and "billing and collection" rules set by HHS

Tax on Innovator Drug Companies 1/10 $22.2B – $2.3 billion annual tax

on the industry imposed relative to share of sales made that year.

Tax on Health Insurers 1/14 $60.1B – Annual tax on the industry imposed

relative to health insurance premiums collected that year. The

stipulation phases in gradually until 2018, and is fully-imposed on

firms with $50 million in profits.

$500,000 Annual Executive Compensation Limit for Health Insurance

Executives 1/13 $0.6B

Employer Reporting of Insurance on W-2 1/11 Min$ – Preamble to taxing

health benefits on individual tax returns.

Corporate 1099-MISC Information Reporting 1/12 $17.1B – Requires

businesses to send 1099-MISC information tax forms to corporations

(currently limited to individuals), a huge compliance burden for small

employers

“Black liquor” tax hike (Tax hike of $23.6 billion). This is a

tax increase on a type of bio-fuel.

Codification of the “economic substance doctrine” $4.5B – This

provision allows the IRS to disallow completely-legal tax deductions

and other legal tax-minimizing plans just because the IRS deems that

the action lacks “substance” and is merely intended to reduce taxes

owed.

Archives

|